FRTB: Internal Model Approach & Risk Modeling

Implementing robust, machine learning-driven risk factor modeling to meet the complex regulatory requirements of the Fundamental Review of the Trading Book.

Business Case

The Fundamental Review of the Trading Book (FRTB) represents a major overhaul of market risk capital requirements. Financial institutions face the significant computational challenge of accurately modeling risk factors to comply with the Internal Model Approach (IMA) and optimize their capital charges.

Outcome

We designed and implemented a Python-based machine learning pipeline to automate risk factor determination and modellability validation, seamlessly providing calculation inputs to the bank's downstream capital charge engine.

Detailed Report

Introduction to FRTB

The Fundamental Review of the Trading Book (FRTB) is a comprehensive suite of capital rules developed by the Basel Committee on Banking Supervision (BCBS). Introduced as a critical pillar of the Basel III framework, FRTB aims to establish a more resilient and standardized market risk framework. Its primary goal is to address shortcomings exposed during previous financial crises, ensuring that banks maintain sufficient capital buffers against market shocks.

Standardised Approach (SA) vs. Internal Model Approach (IMA)

Under the FRTB framework, financial institutions must calculate their market risk capital requirements using one of two methods: the Standardised Approach (SA) or the Internal Model Approach (IMA).

The Standardised Approach is a prescriptive, regulator-defined formula that relies on standardized risk weights. It is highly conservative and serves as both a baseline and a fallback mechanism. In contrast, the Internal Model Approach (IMA) allows banks to use their own proprietary quantitative models and historical data to calculate capital charges. This approach requires strict regulatory approval at the trading desk level and mandates continuous performance and backtesting.

The Objective of the IMA

The main objective of the IMA is to provide a highly risk-sensitive framework. By leveraging a bank’s internal risk management models, the IMA aligns regulatory capital requirements much more closely with the actual, granular economic risks a bank faces. For institutions with sophisticated trading operations, successfully implementing the IMA generally results in a more optimized and accurate capital charge compared to the rigid constraints of the Standardised Approach.

Risk Factor Determination and the SSRM

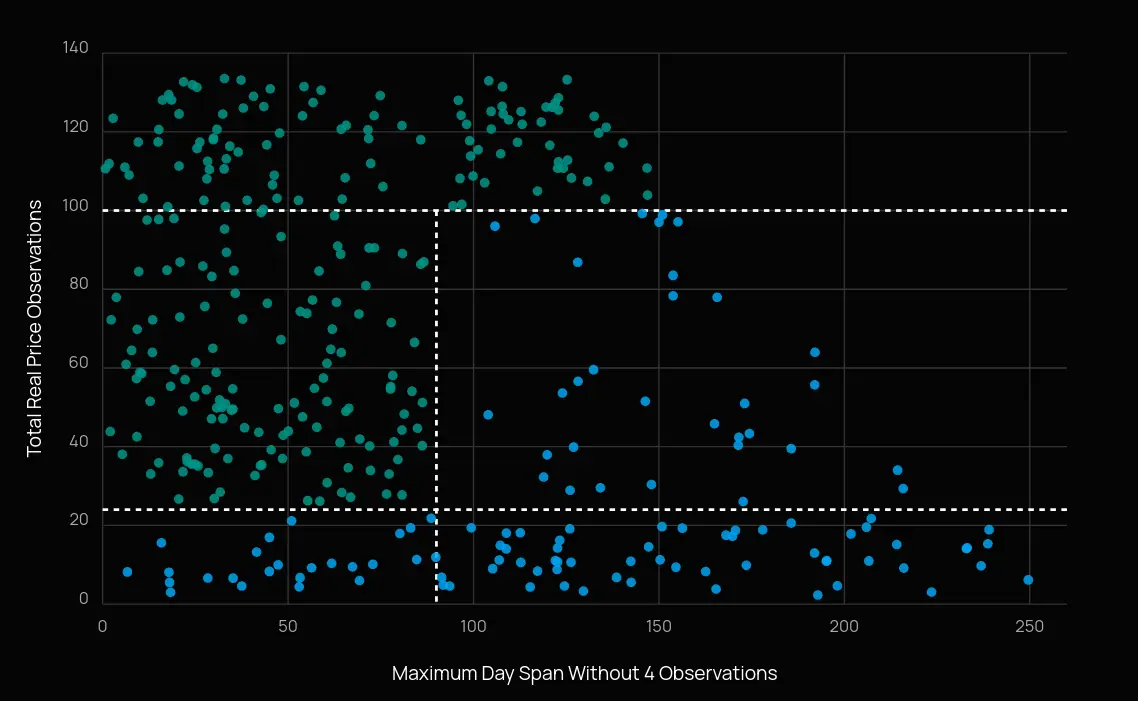

Successfully implementing the IMA is a massive operational and computational undertaking. A significant amount of resources must be invested in determining the risk factors that directly influence the Stressed Scenario Risk Measure (SSRM), which ultimately dictates the final capital charge. Regulators require strict categorization of these risk factors based on the liquidity and observability of the underlying market data.

To demonstrate the complexity of this classification, use the interactive model below to adjust the threshold criteria and observe how it impacts the distribution of Modellable vs. Non-Modellable risk factors.

Capitalizing Non-Modellable Risk Factors (NMRF)

When a risk factor fails the regulatory modellability criteria, it cannot be capitalized using a bank’s standard Expected Shortfall (ES) framework. Instead, financial institutions must pivot to the Stressed Scenario Risk Measure (SSRM). Calculating the SSRM is a highly complex, computationally intensive undertaking designed to penalize data obscurity and ensure sufficient capital buffers for illiquid market variables.

The core of this complexity lies in determining the Extreme Scenario of Future Shock (ESFS). For every individual NMRF, risk engines must scan a continuous 10-year historical observation window to isolate the absolute worst-case upward and downward shocks across prescribed liquidity horizons. Once identified, the entire affected portfolio must be re-priced under this extreme scenario to calculate the maximum potential loss.

This operational burden compounds exponentially during aggregation. To calculate the total Stressed Expected Shortfall (SES), institutions must riggerously prove whether their NMRFs are idiosyncratic (uncorrelated). Idiosyncratic factors benefit from diversification and are aggregated using the square root of the sum of the squares. However, correlated factors—or those lacking sufficient proof of independence—must be aggregated linearly. This simple sum approach offers zero diversification benefit and drastically inflates the final capital charge (the Own Funds Requirement).

How Machine Learning Can Help

Banks usually default to using their own trade data for the IMA model. The regulation allows for third party data when adhering to predefined regulatory standards. The challenge is to determine which trade data asset classes to buy. In order to maximize the return on investment banks want to buy trade data that complements their own data rather than duplicating. Ideally the trade data purchase causes non modellable risk factors to become modellable.

We tackled this intensive process using an advanced Python tech stack

(heavily utilizing pandas, pytorch, numpy and sqlalchemy) combined with Machine Learning

approaches to select respective trade data targets. Furthermore we developed an automated

pipeline that ran the execution of the risk factor shock generation required by the downstream engine to

compute the final capital charge.

Further Reading & Regulatory Literature

For a deeper dive into the quantitative methodologies, proxy fallback mechanisms, and strict regulatory expectations surrounding these calculations, we recommend consulting the official documentation from the European Banking Authority (EBA). The definitive guidelines and formulas governing this framework are outlined in the EBA’s Final draft Regulatory Technical Standards on the calculation of the stress scenario risk measure under Article 325bk(3) of Regulation (EU) No 575/2013 (Capital Requirements Regulation).

Key Regulatory Links:

License

All original content by Henrik Lütjeharms is licensed under a Creative Commons Attribution 4.0 International License.

© 2026 Helionox GmbH.